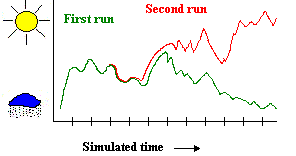

Over 50 years ago, Edward Lorenz created an algorithmic computer weather model at MIT to try to provide accurate weather forecasts. During the winter of 1961, as recounted by James Gleick in Chaos: Making a New Science, Professor Lorenz was running a series of weather simulations using his computer model when he decided to repeat one of them over a longer time period. To save time (the computer and the model were primitive by today’s standards) he started the new run in the middle, typing in numbers from the first run for the initial conditions, assuming that the model would provide the same results as the prior run and then go on from there. Instead, the two weather trajectories diverged on completely separate paths.

Over 50 years ago, Edward Lorenz created an algorithmic computer weather model at MIT to try to provide accurate weather forecasts. During the winter of 1961, as recounted by James Gleick in Chaos: Making a New Science, Professor Lorenz was running a series of weather simulations using his computer model when he decided to repeat one of them over a longer time period. To save time (the computer and the model were primitive by today’s standards) he started the new run in the middle, typing in numbers from the first run for the initial conditions, assuming that the model would provide the same results as the prior run and then go on from there. Instead, the two weather trajectories diverged on completely separate paths.

After ruling out computer error, Lorenz realized that he had not entered the initial conditions for the second run exactly. His computer stored numbers to an accuracy of six decimal places but printed the results to three decimal places to save space. Lorenz had entered the rounded-off numbers for his second run starting point. Astonishingly, this tiny discrepancy altered the end results dramatically.

This finding (even using a highly simplified model and confirmed by further testing) allowed Lorenz to make the otherwise counterintuitive leap to the conclusion that highly complex systems are not ultimately predictable. This phenomenon (“sensitive dependence”) came to be called the “butterfly effect” because a butterfly flapping its wings in Brazil can set off a tornado in Texas. Lorenz built upon the work of late 19th century mathematician Henri Poincaré, who demonstrated that the movements of as few as three heavenly bodies are hopelessly complex to calculate, even though the underlying equations of motion seem simple.

Accordingly and at best, complex systems – from the weather to the markets – allow only for probabilistic forecasts with significant margins for error and often seemingly outlandish and hugely divergent potential outcomes. We can generally accept mild randomness. Whether a particular stoplight is red or green at a given time doesn’t generally change our expectation for how long our commute to work is going to take. But such wild randomness is another matter altogether. Traditional economics has generally failed to grasp the inherent complexity and dynamic nature of the financial markets, which (utterly chaotic) reality goes a long ways towards providing a decent explanation for the 2008-09 real estate meltdown and financial crisis that seem inevitable in retrospect but were predicted by almost nobody.

The “Why?” behind this obvious problem is, it seems to me, bound up in our excessive certainty. We all crave certainty which of course makes our “certain” beliefs self-validating and excessive. A 2005 brain study found that even a little ambiguity on its own lights up the amygdale. The more ambiguity, the more threat response, and the less reward response there was in the ventral striatum. Thus uncertainty is taken as a threat, attracting scarce attention and resources, while certainty is much easier and well-rewarded.

Ultimately, the brain is a prediction machine, constantly considering what happens next while suffering from a sort of information addiction. As Jeff Hawkins argues, “Your brain receives patterns from the outside world, stores them as memories, and makes predictions by combining what it has seen before and what is happening now… Prediction is not just one of the things your brain does. It is the primary function of the neo-cortex, and the foundation of intelligence.” We are thus pattern-recognizers and meaning-makers at every level, constantly.

Accordingly, chaos – which is inherently unpredictable – is often deemed a great enemy to be shunned and thus routinely seen as a malevolent force.

“I try to show the schemers how pathetic their attempts to control things really are.”

Or, at best, chaos — while dangerous — presents great opportunity.

[Watch here; the video cannot be embedded].

“Chaos isn’t a pit. Chaos is a ladder.”

Instead, I want to suggest that chaos isn’t necessarily evil or that it always provides opportunity. It’s just reality.

“Life finds a way.”

If we are to succeed in investing and in life generally, we need to recognize that chaos is an inherent part of life. Sometimes it is a pit to be avoided, sometimes it presents opportunity (Warren Buffett: “Be fearful when others are greedy and greedy when others are fearful”), but it is always there. We need to embrace uncertainty and plan for it as best we can all the while recognizing that we can’t plan for every contingency – not even close. The markets (like the world) are far too complex to be manipulated in that way and to that extent.

Our failings in this regard are as dangerous as they are predictable (and cut both ways) – the planning fallacy writ large. If you can’t take Bob Dylan’s precedent and make chaos a friend, at least accept it as a constant companion, because “it exists and that’s all there is to it.”

Reblogged this on kdwilsonauthorblog.

Pingback: Saturday links: deep exploration | Abnormal Returns

Pingback: Kobayashi Maru and the Forecasting Follies | Above the Market

Pingback: 5 links | Alejandro Lencioni

Pingback: February 11 – A New Kind of Investment Outlook | Prudent Trader

Pingback: A New Kind of Investment Outlook | Thought Equity

Pingback: In Times Like These | Above the Market

Pingback: Here We Go Again: Forecasting Follies 2016 | Above the Market

Pingback: Complexity, Chaos and Chance | Above the Market

Pingback: 2017 Investment Outlook | Above the Market