2015 Outlook

2015 Outlook

Forecasting Follies

Nobody’s perfect.

That universal truth is easy to prove, of course, and no sane person would deny it. Indeed, even the smartest of us are far from immune even in our areas of expertise when we’re actively trying to do our best. A famous study by the U.S. Institute of Medicine concluded that up to 100,000 people die each year due to readily preventable medical errors. Since physicians are among the smartest and most highly trained professionals imaginable, being stupid is obviously not a prerequisite for making mistakes, even horrible mistakes.

It’s also easy to prove how error-prone we are in the investment world. Every year I take a look at various predictions for the year that’s ending and they are uniformly lousy in the aggregate. Moreover, when somebody does get one right or almost right, that performance quality is not repeated in subsequent years.

2014 provided more of the same in this regard. The median S&P 500 forecast among 50 top-end investment experts called for a year-end level of 1,950, up 6.44 percent on the year. As noted above, the actual closing level was 2,059, up 11.39 percent, essentially five full percentage points higher. That’s a miss of monumental proportions.

Last January, analysts called for far higher oil prices, firmer inflation, a worse jobless rate and higher interest rates. The exact opposite happened in each of those areas. The consensus crude oil price forecast was nearly $95 per barrel (up a bit) and 72 out of 72 economists were anticipating higher interest rates and lower bond prices. Advisor magazine reported that bond market sentiment was utterly bearish, leading pundits to recommend that investors limit their bond holdings to the shortest maturities in 2014. Meanwhile, 30-year U.S. Treasury bonds returned nearly 30 percent. Last April, Peter Schiff of EuroPacific Capital made the bold prediction that the “Federal Reserve’s quantitative-easing program will push gold to $5,000 an ounce.” The shiny yellow metal closed 2014 at just under $1,200, 80 percent or so lower than Schiff’s target.

Alleged experts miss on their forecasts and miss by a lot. Let’s stipulate that these alleged experts are highly educated, vastly experienced, and examine the vagaries of the markets pretty much all day, every day. But it remains a virtual certainty that they will be wrong often and often spectacularly wrong. On account of hindsight bias, we tend to see past events as having been predictable and perhaps inevitable. Accordingly, we think we can extrapolate from them into the future. But the sad fact is that we can’t buy past results.

For what it’s worth, individual investors did even worse. The S&P 500’s total return of roughly 14 percent this year was 40 percent higher than its 25-year average annual gain. It printed over 50 all-time record closes. But according to MSN Money and its annual survey of Main Street retail investors — as opposed to Wall Street pros — individual investors came up with an average 2014 forecast that U.S. stocks would decline “at least” 10 percent for the year, a wild miss of nearly twenty-five percentage points. It would have been hard to have missed by more (unless you were John Paulson – see below).

It’s no wonder then that Nassim Taleb tells a sardonic story about forecasting. As the tale goes, a trader listened to the firm’s chief economist provide a forecast about the markets and then lost a bundle acting on it, getting him fired. The trader angrily asked his boss why he was fired rather than the economist, as the economist’s poor forecast led to the poor trade. The boss replied, “You idiot, I’m not firing you for losing money. I’m firing you for listening to the economist.”

To be fair, the current dreadful results aren’t at all unusual. Market forecasting has a long and ignominious history. Irving Fisher was a noted 20th century economist. No less an authority than Milton Friedman called him “the greatest economist the United States has ever produced.” But just three days before the famous 1929 Wall Street crash (timing is everything) he claimed that “stocks have reached what looks like a permanently high plateau.” Similarly, on March 6, 2009, Michael Boskin argued that “Obama’s Radicalism Is Killing the Dow.” Stocks bottomed just three days after publication (timing is everything) and the Dow has gained over 171 percent since, through the end of 2014.

Since 1990, the Federal Reserve Bank of Philadelphia has conducted a quarterly Survey of Professional Forecasters, continuing research conducted from 1968-1989 by the American Statistical Association and the National Bureau of Economic Research. The survey asks various economic experts their views of the probabilities of recession for each of the following four quarters and comes up with an “Anxious Index” reflecting those asserted probabilities.

A CXO study of that data determined that the forecasted probability of recession for a quarter explained absolutely none of the stock market’s returns for that quarter. In fact, the data suggests that the forecasts were a mildly (if not materially) contrarian indicator of future U.S. stock market behavior. In other words, you’d be better off doing the opposite of what the experts suggested than following their advice! The lousy track records highlighted by CXO are entirely consistent with a long line of research (most prominently from Philip Tetlock) establishing the lack of value provided by so-called “expert” forecasters. Forecasting is like Anchorman’s Ron Burgundy leaping into the bear pit and exclaiming, “I immediately regret this decision.”

The market predictions offered by experts (and others) and the thought processes underlying them can be very entertaining indeed. They are even the engine that drives much of what pretends to be financial and business television. But none of us should take them seriously. Doing so would be very dangerous indeed. Based upon the historical record (and the 2014 record!), it’s a good thing that so few bother to hold people accountable for their forecasts. The bottom line here is that anyone who thinks it’s possible to predict the future in the markets ought to think again. Your crystal ball does not work any better than anyone else’s.

Sadly, such dreadful forecasting performance is indicative of dreadful investment performance. The vast majority of investment strategies are predicated upon the ability to forecast the future. These results are no better than the forecasts. As long-time chair of the Yale Endowment Charles Ellis outlines it, research on the performance of institutional portfolios shows that after risk adjustment, 24 percent of funds fall significantly short of their chosen market benchmark and have negative alpha, 75 percent of funds roughly match the market and have zero alpha, while well under one percent achieve superior results after costs—a number not statistically significantly different from zero, largely due to fees. To pick one particularly egregious example among many, hedge funds — despite (and partly because of) enormous fees — have badly underperformed. Since 1998, the effective return to hedge fund clients has barely been 2% per year, half the return they could have achieved simply by investing in Treasury bills.

Thus, per Nassim Taleb, successful managers have risen “to the top for no reasons other than mere luck, with subsequent rationalizations, analyses, explanations, and attributions.” In other words, we desperately pull money from our latest poorly performing strategy to put it into some new approach that has been doing great, only to see the same pattern repeat itself. Sound familiar? John Paulson achieved great notoriety for betting against the real estate markets ahead of the 2008-2009 financial crisis and accumulated billions of investor dollars into his hedge fund as a result, only to get crushed in 2014, losing 36 percent in his Advantage Plus fund despite a very strong market environment.

Not only is it really hard to beat the market overall, but when you do make a smart investing move (purchasing an investment that will actually outperform, however you define that), its impact is reduced every time somebody else follows suit. It is axiomatic in the investment world that as an asset class becomes more popular, it suffers from both falling expected returns and rising correlations. Good trades get crowded and their advantages tend to disappear. Crowding occurs because success begets copycats as investors chase returns. General mean reversion only tends to make matters worse.

In other words, the more smartness there is in the aggregate, the less you can profit from it. Michael Mauboussin describes it as the paradox of skill: “As skill improves, performance becomes more consistent, and therefore luck becomes more important.” Accordingly, those (very) few funds and managers that have a successful long-term track record end up outperforming their peers by precious little indeed.

On the other hand, the impact of bad decision-making stands alone. It isn’t lessened by the related stupidity of others. In fact, the more people act stupidly together, the greater the aggregate risk and the greater the potential for loss, which grows exponentially. Think of everyone piling on during the tech or real estate bubbles. When nearly all of us make the same kinds of mistakes together — when the error quotient is really high — the danger becomes enormous.

Perhaps worst of all, the returns achieved by investors are even lower than those obtained by managers because we are enslaved by our emotions and poor decision-making (see the charts below). When something isn’t right (or doesn’t seem right), our default response is to do something. And what we do is to insist on buying what was just hot and selling what has just underperformed, guaranteeing that we buy high and sell low, which is exactly what we shouldn’t do.

We all want “high leverage” ideas – the ideas that will make the biggest impact on our portfolios and our lives. But the best ideas available are not still more investment recommendations about hot sectors, hot funds, hot strategies and hot managers. There is no reason to think anybody can do that anyway. The best ideas I can offer relate to our besetting mistakes, mistakes we make over and over again. The answer is to get off the merry-go-round of the next new thing and to eliminate our obvious mistakes first and foremost.

My High Leverage Idea: Eliminate Obvious Mistakes

It simply doesn’t make a lot of sense to spend enormous amounts of time and energy looking for a strategy or a manager that might (but probably won’t) outperform by just a little bit. It makes a lot more sense to eliminate the mistakes – often very big mistakes – that make success so very hard for us to achieve. As the great Spanish artist Pablo Picasso put it, “Every act of creation is first of all an act of destruction.” What we want to do is to find the next great investor, the terrific new strategy, the market sectors that are about to heat up or the next Apple. That’s what traditional investment outlooks set out to do. But what we should do is eliminate the big mistakes that make it so hard for us to get ahead. That’s what I’ll try to help you do instead.

As Charley Ellis famously established, investing is a loser’s game much of the time, with outcomes dominated by luck rather than skill and high transaction costs. Thus if we avoid mistakes we will generally win. As Phil Birnbaum brilliantly suggests in Slate, not being stupid matters demonstrably more than being smart when, as in investing, a combination of luck and skill determines success. “You gain more by not being stupid than you do by being smart. Smart gets neutralized by other smart people. Stupid does not.”

This principle can be demonstrated mathematically, as Birnbaum notes. Gather 10 people and show them a jar that contains equal numbers of $1, $5, $20, and $100 bills. Pull one out, at random, so nobody can see, and auction it off. If the bidders are generally smart, the bidding should top out at just below $31.50 (how much less will depend on the extent of the group’s loss aversion), the value of the average bill {(1+5+20+100)/4}.

If you repeat the process but this time let two prospective bidders see the bill you picked, what happens? If you picked a $100 bill, the insiders should be willing to pay up to $99.99 for the bill. Neither of them will benefit much from the insider knowledge. However, if it’s a $1 bill, neither of the insiders will bid. Without that knowledge, each of the insiders would have had a 1-in-10 chance of paying $31.50 for the bill and suffering a loss of $30.50. On an expected value basis, each gained $3.05 from being an insider. It thus matters more to our investment success that we avoid errors than that we make smart investment choices.

But even having this knowledge doesn’t always help. We humans don’t want accuracy nearly so much as we want reassurance. As reported by Jason Zweig in The Wall Street Journal, the Nobel laureate Kenneth Arrow did a tour of duty as a weather forecaster for the U.S. Air Force during World War II. Ordered to evaluate mathematical models for predicting the weather one month ahead, he found that they were worthless. When he reported his findings, his superiors sent back another order: “The Commanding General is well aware that the forecasts are no good. However, he needs them for planning purposes.”

Luck (randomness) is a huge factor in investment returns, irrespective of manager. But we like to think that intelligence and effort can overcome the vagaries of the markets. That’s largely because we are addicted to certainty. That explains, for example, the popularity of the color-by-numbers television procedural, wherein the crime is neatly and definitively solved and all issues related thereto resolved in an hour (nearly a quarter of which is populated with commercials). As television critic Andy Greenwald explains, these crime dramas are “selling the gruesomeness of crime and the subsequent, reassuring tidiness of its implausibly quick resolution.”

I’ve gone to a lot of trouble to show unequivocally that nobody’s remotely close to perfect in the investment world. In fact, very few people are very good. Yet we all like to think that we’re the exception to the rule. We screw up repeatedly and then insist we knew it all along. We even forget (or ignore) how poorly our investments have actually done.

To paraphrase the philosopher Immanuel Kant, the first task of reason is to recognize its limitations. Every rational person acknowledges that they make and have made many errors. Even so, nobody offers current examples. We all want to think that our mistakes are in the past, that we’ve learned from them and that now we’ve set things right. We desperately want to believe that our new approach, new strategy or new portfolio will – finally – be the magic elixir that will make us very good, if not great investors (or at least that we can find those great investors).

As Tim Richards explains, we are both by design and by culture inclined to be anything but humble in our approach to investing. We invest with a certainty that we’ve picked winners and sell in the certainty that we can re-invest our capital to make more money elsewhere. But we are usually wrong, often spectacularly wrong. These tendencies come from hard-wired biases and also from emotional responses to our circumstances. But they also arise out of cultural requirements to show ourselves to be confident and decisive. Even though we should, we rarely reward those who show caution in the face of uncertainty.

We love confident certainty and a tidy resolution. We so badly want to believe that we have (finally) figured out the path to investment success that we keep making the same mistakes over and over again. The great Russian writer Fyodor Dostoyevsky offers a better approach: “Above all, don’t lie to yourself. The man who lies to himself and listens to his own lie comes to a point that he cannot distinguish the truth within him, or around him, and so loses all respect for himself and for others.” This was the choice offered in The Matrix: You can swallow the red pill or the blue pill.

The blue pill maintains the illusion of control, the investment status quo. Very few of us opt for the red pill, preferring the comfortable fantasy over harsh reality. What follows is an outline of how we might choose the red pill.

Choosing the “Red Pill”: Fixing a “Top Ten” List of Mistakes

Princeton’s Burton Malkiel proclaims the stark reality. “There isn’t anybody who can tell you what’s the best asset class for 2015. Nobody. I’ve never known anybody who can time the market. I’ve never known anybody who knows anybody who can consistently time the market.” The investment management business is nostalgic for a past that hasn’t existed for a long time (if it ever has) – a past of great returns and great pay. However, as Andy Greenwald puts it, nostalgia is an indulgence but history is a tidal wave. The tidal wave of history demands that we do things differently. It ought to start by putting aside the quest for investing’s holy grail, even if temporarily, and eliminating the mistakes that so obviously beset us. Conor Oberst, in a song that made many 2014 “best of” lists, expressed it poetically.

Princeton’s Burton Malkiel proclaims the stark reality. “There isn’t anybody who can tell you what’s the best asset class for 2015. Nobody. I’ve never known anybody who can time the market. I’ve never known anybody who knows anybody who can consistently time the market.” The investment management business is nostalgic for a past that hasn’t existed for a long time (if it ever has) – a past of great returns and great pay. However, as Andy Greenwald puts it, nostalgia is an indulgence but history is a tidal wave. The tidal wave of history demands that we do things differently. It ought to start by putting aside the quest for investing’s holy grail, even if temporarily, and eliminating the mistakes that so obviously beset us. Conor Oberst, in a song that made many 2014 “best of” lists, expressed it poetically.

If someone says they know for certain

They’re selling something certainly

Let’s look at the mistakes that so routinely undermine us and make our investment choices and outcomes so disappointing. Most investment outlooks offer a list of favored investments for the coming year. Instead, here is a different sort of “top ten” list of interrelated investment insights and recommendations – mistakes that are both common and deadly – for us to try to correct for 2015 and beyond.

1. We don’t prioritize properly in financial planning.

Your savings rate is far more important than your rate of return in determining how bright your future is likely to be. However, we are far more likely to obsess over squeaking out a bit more performance out of our investments rather than thinking about ways to save more. The following ordered list is a good place to start prioritizing issues to manage your financial future (it’s adapted from here).

- Invest in your company’s 401(k) or comparable (e.g., 403(b)) plan, if you have one, up to the company match; it’s free money.

- Make sure you have adequate insurance coverage based upon your family’s needs.

- Pay off short-term, non-tax-deductible debt (e.g., credit card, car loan).

- Establish an emergency fund; 3-6 months of living expenses is a good guideline (to be adjusted based upon how secure your job is).

- Put the maximum allowable amount in a Roth IRA.

- Put the maximum allowable amount in your company 401(k) or comparable plan.

- Invest the remainder in taxable accounts.

- Pay down tax-deductible debt (e.g., home mortgage).

- Don’t peek at your results (too often).

2. We complicate things unnecessarily.

Einstein wisely advised that we keep things as simple as possible, but no simpler. Overly complicated systems, from financial derivatives to tax systems, are difficult to comprehend, easy to exploit, and possibly dangerous. Simple rules, in contrast, can make us smart and create a safer world.

Einstein wisely advised that we keep things as simple as possible, but no simpler. Overly complicated systems, from financial derivatives to tax systems, are difficult to comprehend, easy to exploit, and possibly dangerous. Simple rules, in contrast, can make us smart and create a safer world.

But, as NASA’s Gavin Schmidt explains, the world we live in is really complex. Similarly, the interworkings and interrelationships of the markets are really complex. It is natural for us to ask simple questions about complex things, and many of our greatest insights have come from the profound examination of such simple questions. “However, the answers that have come back are never as simple. The answer in the real world is never ‘42’.”

Still, we keep acting as though simple answers always exist. It’s easy to find investment managers eager to explain how they’ve found “it,” how they’ve calculated the complexities and vagaries of the markets and come up with “42” (or at least that the right answer is between 40 and 44). We cling to the idea that the investment markets can be solved. Only charlatans claim to have done so, and maintain the charade by hiding behind unnecessary complexity.

3. We don’t invest.

The stock market is scary. Investing there requires that we be prepared for major losses as serious drawdowns are part of the package (see below).

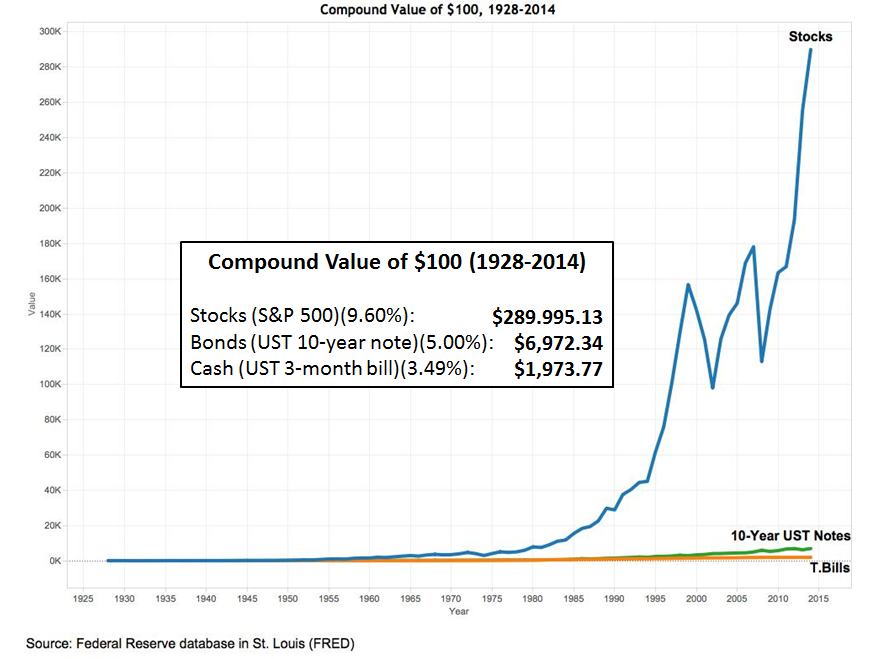

A broad index of U.S. stocks increased 2,000-fold between 1928 and 2013, but lost at least 20 percent of its value 20 times during that period. People might be less scared of volatility if they knew how common it was. Some people react to the reality that markets go down sometimes and sometimes by a lot by avoiding stocks altogether. But doing so is a huge mistake. One chart makes the case unequivocally (see below).

That’s right. It’s not a misprint. The difference is astronomical.

And if you think that the chart doesn’t really paint an accurate picture because things are different now somehow, let’s have a look at just the last ten years, which allows us to include so-called “alternative investments.”

Same story. Despite an historically bad stock market crash, an historically great environment for bonds, and huge interest in alternatives, stocks win easily. If you want your investment portfolio to perform, you have to include a healthy dose of stocks. There’s no way around it.

4. We don’t stay invested.

Out of our general fear, even if and when we invest, we often don’t stay invested.

The above chart, verified to me as still accurate through 2014 by Morgan Housel, demonstrates that if we have the wherewithal to keep our composure during difficult markets, we will be rewarded for it.

According to University of Oregon economist Tim Duy, “As long as people have babies, capital depreciates, technology evolves, and tastes and preferences change, there is a powerful underlying impetus for growth that is almost certain to reveal itself in any reasonably well-managed economy.” Numerous studies have shown that those who trade the most earn the lowest returns. Remember Pascal’s wisdom: “All man’s miseries derive from not being able to sit in a quiet room alone.” Overtrading is indeed a big killer of returns. As finance researchers Brad Barber and Terry Odean show in a landmark 2000 paper, “trading is hazardous to your wealth.” Yet our instinctive reaction to every market correction or downturn is to change something and almost always to sell something.

As David Rosenberg explains, “Corrections are part and parcel of the investment process, they come and go, and it is imperative to take a deep breath and realize that what is most important for building wealth is not ‘timing’ the market but rather ‘time in’ the market.” It pays to stay invested. So please listen to Wesley Gray: “You can lead an investor to a winning strategy, but you can’t make them stick with it when the going gets tough. Unfortunately, success comes at a steep price. You need to be willing to sit through periods of downright dreadful performance. No risk, no reward. It really is that simple.”

5. We don’t diversify.

According to the Uniform Prudent Investor Act, “Because broad diversification is fundamental to the concept of risk management, it is incorporated into the definition of prudent investing.” The theory behind diversification is simple: Don’t put all of your eggs in one basket. A single holding has huge potential for gains if the right instrument is selected, but even huger risks (because investing “home runs” are so hard to come by). In general, the greater a portfolio’s diversification, the lower its risk. Lower risk is a good thing, but only if the portfolio’s potential return is healthy enough to meet the client’s needs. Fortunately, a well-diversified portfolio captures most of the potential upside available with much lower volatility.

According to the Uniform Prudent Investor Act, “Because broad diversification is fundamental to the concept of risk management, it is incorporated into the definition of prudent investing.” The theory behind diversification is simple: Don’t put all of your eggs in one basket. A single holding has huge potential for gains if the right instrument is selected, but even huger risks (because investing “home runs” are so hard to come by). In general, the greater a portfolio’s diversification, the lower its risk. Lower risk is a good thing, but only if the portfolio’s potential return is healthy enough to meet the client’s needs. Fortunately, a well-diversified portfolio captures most of the potential upside available with much lower volatility.

A diverse portfolio – one that reaches across all market sectors – ensures that at least some of a portfolio’s investments will be in the market’s stronger sectors at any given time – regardless of what’s hot and what’s not and irrespective of the economic climate. At the same time, a diverse portfolio will never be fully invested in the year’s losers. For example, according to Morningstar Direct, about 25% of U.S. listed stocks lost at least 75 percent of their value in 2008 but only four of over 6,600 open-ended mutual funds lost more than 75 percent of their value that year. Thus a diversified approach provides much smoother returns over time (even if not as smooth as desired!). On the other hand, a well-diversified portflio will always include some poor performers, and that’s hard for us to abide.

The table immediately above will be familiar to most of you. It shows the annual returns of various asset classes over the past decade. Most people pick investments based upon what is “hot.” If, over that period, one had invested in the previous year’s top performer each year, s/he would have received 2.73 percent average annual returns. But since investing tends to be mean reverting, a contrarian who invested in the previous year’s worst performer would have averaged returns of 6.5 percent, well over twice as high. Even so, an investor who created the more diversified (if not optimal) asset allocation portfolio outlined above would have seen even better average annual returns still – 7.25 percent.

We like the idea of diversification much more than the reality because diversification is hard. If a portfolio doesn’t have assets that are doing poorly, it isn’t well diversified. Diversification is painful. But it’s healthy.

6. We value investment choices over asset allocation.

A portfolio’s results are largely dictated by overall market performance during any given time period. In other words, the more risk-averse strategies will generate better returns in a difficult market by protecting the downside and the reverse will also tend to be true, that managers with higher risk tolerances will be more likely to succeed during periods of strong market returns. The conventional method of mitigating this dilemma is to “risk adjust” the results, comparing nominal returns with volatility, but this approach is uncertain at best in that volatility and risk are hardly the same thing.

The total return of any portfolio has three components, which may be positive or negative: (a) returns from overall market movement; (b) incremental returns due to asset allocation; and (c) returns due to timing, selection, and fees (active management). The latest research suggests that, in general, about three-quarters of a typical portfolio’s variation in returns comes from market movement (a), with the remaining portion split roughly evenly between the specific asset allocation (b) and active management (c). To the extent that research differs from that stated above, it concludes that asset allocation is more important and active management is less important.

The exercise of allocating funds among various investment vehicles and asset classes is at the heart of investment management. Asset classes exhibit different market dynamics and different interaction effects. Thus the allocation of money among asset classes and among investment vehicles within asset classes will have a significant effect on the performance of the investment portfolio.

The primary skill of a successful investment manager resides in constructing the asset allocation, and separately the individual holdings, so as to meet the client’s needs. Therefore, we should spend at least as much time and care in constructing a diversified asset allocation plan as on the investment vehicles used to execute the asset allocation decision. Establishing a well diversified asset allocation plan consistent with one’s goals, investment horizon, and risk tolerance should be a major priority. For most of us, it is not.

7. We try to time the market.

The idea that an in investor ought to be aware and nimble enough to avoid market downturns or simply to find and move into better investments is remarkably appealing. Just show me any who have done it repeatedly. For example (and as noted above), John Paulson achieved great notoriety for betting against the real estate markets ahead of the 2008-2009 financial crisis and drew billions of dollars to his hedge fund as a result, only to get crushed in 2014, losing 36 percent in his Advantage Plus fund despite a very strong market environment. A growing body of research is unequivocal in finding that chasing returns is a killer for investors. Last year, investment strategist Gerard Minack studied the timing and volumes mutual fund flows to see how investors’ actual returns compared to movements in the market. As expected, he found that inflows became most aggressive as markets peaked and outflows ramped up when markets were near their lows.

The idea that an in investor ought to be aware and nimble enough to avoid market downturns or simply to find and move into better investments is remarkably appealing. Just show me any who have done it repeatedly. For example (and as noted above), John Paulson achieved great notoriety for betting against the real estate markets ahead of the 2008-2009 financial crisis and drew billions of dollars to his hedge fund as a result, only to get crushed in 2014, losing 36 percent in his Advantage Plus fund despite a very strong market environment. A growing body of research is unequivocal in finding that chasing returns is a killer for investors. Last year, investment strategist Gerard Minack studied the timing and volumes mutual fund flows to see how investors’ actual returns compared to movements in the market. As expected, he found that inflows became most aggressive as markets peaked and outflows ramped up when markets were near their lows.

As my friend Josh Brown pointed out in Fortune, just five stocks—Apple, Berkshire Hathaway, Johnson & Johnson, Microsoft, and Intel— accounted for roughly 20 percent of the market’s gains and only 30 percent of S&P 1500 stocks posted gains exceeding the index itself in 2014. According to data compiled by Bloomberg, hedge funds were up an average of just 2 percent on the year. Once the final numbers are in, over 1,000 funds will likely have closed down in 2014. Meanwhile, of the top three tactical strategies in the country (Mainstay Marketfield, Good Harbor U.S. Tactical Core, F-Squared Premium AlphaSector Index), two nearly imploded with big losses while the third found itself in trouble with the SEC for misleading the public about its historical returns. The other giant tactical fund, Schwab’s $9 billion Windhaven Diversified Growth product, ended 2014 with both lousy returns and shrinking assets under management. So much for tactical management (the more recent name for market timing).

Whatever one thinks of his favored economic policies, John Maynard Keynes was, by any measure, one of the great investors of all time. Yet even he did poorly until he gave up trying to time the market. Warren Buffett doesn’t even try.

If you stop to think about it, the idea that anyone should expect to be able successfully to time the market is nuts because you have to be right about so many things at the same time to do so. We’ve already seen how badly we all are at trying to forecast the macro environment or even its component parts – no expert (literally!) predicted that oil would take the beating it has over the past several months, for example. Then you have to get the theme right (rising rates, higher inflation, etc.). Almost nobody does that either. And then you need to pick the vehicles that will work the best in your chosen scenario. Success is highly unlikely. So you should avoid the error of trying.

We’ve all seen it and done it. We find a hot new approach or hot new manager and, because what we own hadn’t been doing so well, we switch, only to find that the hotness that had caused us to buy cooled. We need to get off that merry-go-round.

8. We fail to consider costs.

The leading factor in the success or failure of any investment is fees. In fact, the relationship between fees and performance is an inverse one. Every investor needs to count costs.

The leading factor in the success or failure of any investment is fees. In fact, the relationship between fees and performance is an inverse one. Every investor needs to count costs.

9. We fail to consider incentives.

Multiple studies all establish what we should already know. A manager with a significant ownership stake in his fund is much more likely to do well than one who doesn’t. Make sure to look for “skin in the game” from every money manager you use.

Multiple studies all establish what we should already know. A manager with a significant ownership stake in his fund is much more likely to do well than one who doesn’t. Make sure to look for “skin in the game” from every money manager you use.

10. We try to go it alone.

American virologist David Baltimore, who won the Nobel Prize for Medicine in 1975 for his work on the genetic mechanisms of viruses, once told me that over the years (and especially while he was president of CalTech) he had received many manuscripts claiming to have solved some great scientific problem or to have overthrown the existing scientific paradigm to provide some grand theory of everything. Most prominent scientists have drawers full of similar submissions, almost always from people who work alone and outside of the scientific community. Unfortunately, none of these offerings has done anything remotely close to what was claimed, and Dr. Baltimore offered some fascinating insight into why he thinks that’s so. At its best, he noted, good science is a collaborative, community effort. On the other hand, crackpots work alone.

American virologist David Baltimore, who won the Nobel Prize for Medicine in 1975 for his work on the genetic mechanisms of viruses, once told me that over the years (and especially while he was president of CalTech) he had received many manuscripts claiming to have solved some great scientific problem or to have overthrown the existing scientific paradigm to provide some grand theory of everything. Most prominent scientists have drawers full of similar submissions, almost always from people who work alone and outside of the scientific community. Unfortunately, none of these offerings has done anything remotely close to what was claimed, and Dr. Baltimore offered some fascinating insight into why he thinks that’s so. At its best, he noted, good science is a collaborative, community effort. On the other hand, crackpots work alone.

Similarly, the idea of a lone genius changing the world is also a myth. As The Los Angeles Times reported about Bill Gross and PIMCO, “In the wake of [Mohammed] El-Erian’s departure, stories leaked out about Gross’ imperious behavior – traders were forbidden to speak to him or even make eye contact on the trading floor, the Wall Street Journal reported. He brooked no discussion or debate about his trading strategies and became hostile to rising talents on the floor.” Whether we’re talking about Lennon and McCartney or Warren Buffett and Charlie Munger, we all work better with help, advice, support, correction, criticism and accountability. Make sure you aren’t trying to go it alone in the investment world.

Similarly, the idea of a lone genius changing the world is also a myth. As The Los Angeles Times reported about Bill Gross and PIMCO, “In the wake of [Mohammed] El-Erian’s departure, stories leaked out about Gross’ imperious behavior – traders were forbidden to speak to him or even make eye contact on the trading floor, the Wall Street Journal reported. He brooked no discussion or debate about his trading strategies and became hostile to rising talents on the floor.” Whether we’re talking about Lennon and McCartney or Warren Buffett and Charlie Munger, we all work better with help, advice, support, correction, criticism and accountability. Make sure you aren’t trying to go it alone in the investment world.

Conclusion

It’s a key part of the gig. Everyone in a job like mine is supposed to offer at least an annual investment outlook and that outlook is supposed to include a listing of my best investment ideas, meaning where I think you should put your money to have the best opportunity for the biggest gains in the coming year. In other words, I’m supposed to like Apple or small caps or European stocks. But that approach isn’t thinking like a smart investor.

A smart investor looks for what can be done that offers the greatest opportunity for success in the markets. But finding and implementing these best ideas is deceptively easy conceptually yet monumentally hard to put into practice. Let’s start by systematically eliminating our most obvious mistakes. The more we do that, the better 2015 can turn out to be, irrespective of what the markets do.

Reblogged this on The Safe Investing Blog.

Reblogged this on A rose by any other name would smell as sweet and commented:

A very good “Long Read”. Lot of Wisdom out here.

Pingback: February 11 – A New Kind of Investment Outlook | Prudent Trader

Pingback: 02/11/15 - Wednesday AM Interest-ing Reads -Compound Interest Rocks

I wish I could get a printable version of this so I could reread it once a month (at least).

Pingback: What Do Low Interest Rates Mean for Stock Market Returns? - A Wealth of Common SenseA Wealth of Common Sense

Pingback: Weekly market round-up: 16 February 2015 | Dustin's Blog

Agree with Bil. Going to print out and read once a month!

Reblogged this on Financial Markets.

Great read 😀 I’m totally with you in the erring principle.

Pingback: Michael Covel Podcast | Above the Market

Reblogged this on Seeking Profits.

Pingback: Make Fewer Decisions | Above the Market

Pingback: Beating the Bias Trap (Additional Resources) | Above the Market

Pingback: Pants on Fire: 10 Big Lies in the Financial Services Industry | Above the Market

Pingback: What’s On Your Mind? Investor Questions

Pingback: Happy Blogiversary to Me | Above the Market

Pingback: Discounting the economic consensus | Financial Post

Pingback: ILAB 103 - After the Big Exit - Investing Philosophy and Life Optimization with David Hauser - Invest Like a Boss